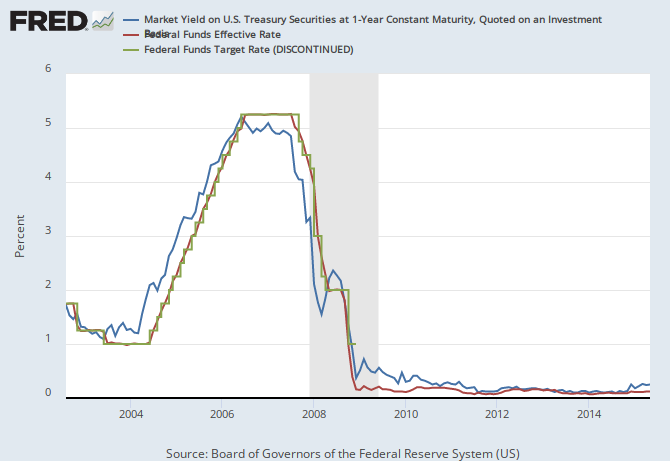

There is only one member bank, Jack Lew and Goldman Sachs. The other banks and the Fed simply wait for instructions. If the Fed and member banks were doing true price discovery, then that variance between the effective rate, the target and the one year would be about the same. What we have is mickey mouse from the MIT basket Weavers.

Here is a reference: http://www.newyorkfed.org/markets/omo/omo2007.pdf

here are some numbers. The total float is %8 billion, and the banks stay within 25 basis points, YoY. Given 30 member banks, that comes to about 900k per year in savings for that accuracy, and the trader to manage that will cost some 500k per year! No, this is not accurate price discovery, this is simply member banks awaiting instructions from Goldman Sachs who manages the debt flow for Jack Lew.

No comments:

Post a Comment