We did borrow, the ten year was 3.5% for two years after the crash. Romer and the Berkeley bozos could not borrow enough money at those rates.

Now we are rolling over that debt at 2% and getting some releif. Our interest costs on that debt, and the prior debt should drop by 40% over the next three years. That is a savings of about $100 billion/yr, at least, in money the Berkeley bozos sent back to the super wealthy.

I claim, once again, it is time to shut down the UC Berkeley economics department.

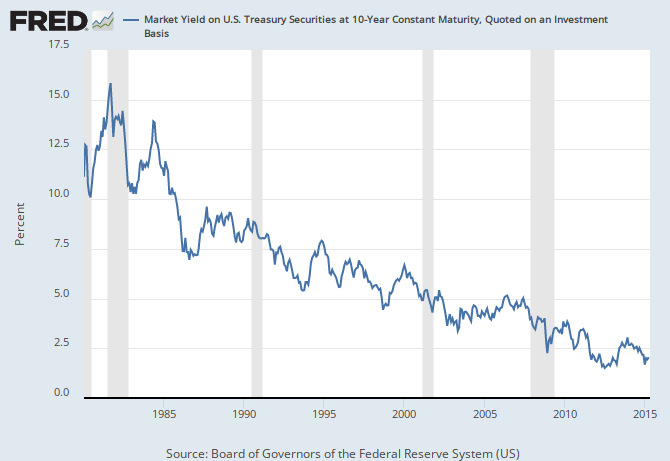

What is the other horse manure I keep hearing? Oh yes, inflation helps the debtor. Not when the debtor is rollin over almost 2 trillion a year. Look backwards you incompetent economists, almost the entirety of the US government debt was borrowed, almost always, at higher rates in the past. Do you bozos need a chart? Ok, but as near as I can tell the Kanosian boneheads never look at them, here it is:

But wait, the boneheads will say, we pay back in cheaper dollars. Not unless they can show taxes going up faster than rates with inflation. And they cannot, and will not. They are limited to reading recipes, mostly from the MIT Basket Weavers.

Here is one more. Look at those gray bars. Where do they occur? At eight year presidential boundaries. All of them, with the exception of Reagan who caused a massive grey bar about six month after entering office. Now, mathematicians, what would you tell you college president if you knew that almost every economist, except Roger Farmer, cannot find the cycle? Every one of our bonehead Kanosians go into their classrooms, put up this chart, and claim DC is counter cyclical! Mathematicians you need to move these folks off of campus, and take over the business of aggregate statistics.

No comments:

Post a Comment