This convinces me that staying with the near-zero interest rate policy alone--and promising to stay near-zero for a long time without doing anything else--risks a deflationary trap.Bullard is refering to a paper he has, Seven Faces of Peril

Let me give my summary. The bankers yield curve is generally six months from maximum entropy. If the real economy is adjusting, no problem, the yield curve still gives future gains from restructuring that is pending. Easy to see. Maximum entropy has fewer solutions and investors can easily choose the proper curve that generates potential growth.

Bullard is wrong about QE, the proper solution is to target the shape of the yield curve. QE is popular because it is a fraud to avoid the pestering from Congress. The Fed should select sample a rate and target a term having half that rate. Pick a sample rate just into the zero area, and the idea is to feed high frequency activity into the curve, forcing the curve to accommodate extra bandwidth at the expense of steepness. Using Nyquist sampling removes the side betting yet retains ambiguity, allowing the economy to adjust at a natural pace.

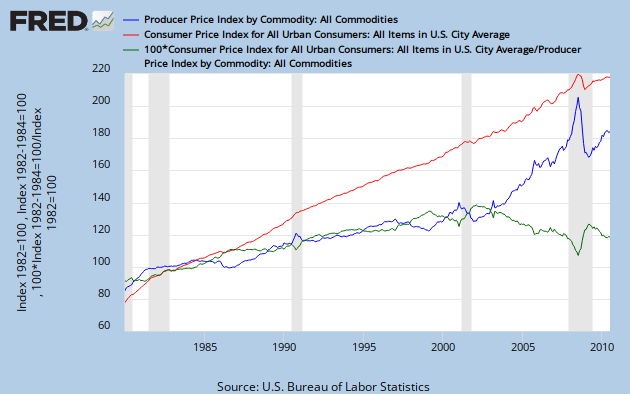

Also, looking at interest rates and inflation from that paper what do I see? A validation of the Kling hypothesis.

HT To economists who ban me from their site.

I am interested in seeing how the Thoma commenters wiggle out of this conclusion because Bullard was a favorite over at Keynesian City.