The model I use is that the vacuum is a bandwidth limited, optimally congested Huffman encoder. lets break that down a bit. Newton though the vacuum had infinite bandwidth. Thermo dynamicists accepted that and said entropy was increasing. Einstein said the the bandwidth was limited. Plank measured the natural uncertainty of congested systems.And quantum physics said that increasing entropy was really increasing mutual entropy which carried action at a distance.

Consider that the vacuum's job is to measure a disturbance, and quantize the disturbance so the probability of two disturbed components colliding was small, and the vacuum was band limited. As the number of samples of the disturbance increase, the vacuum takes out the common components, and quantizes that commonality as quantized mutual entropy, and physicists can go look for it.

The effect of finding the mutual entropy is to encode the disturbance with greater accuracy, more information quantized over the existing number of samples. It finds the common effects when the disturbance becomes congested, and cannot be described within the bandlimit. The more it performs the task, the remaining disturbance is less congested, approaching the optimum congestion.

Thus the action at a distance. Unknown to the experimenter, the vacuum has already measured a disturbance to the optimal congestion level, but the experimenter cannot measure the mutual entropy field, he has not yet discover it. Hence, to the limit of the natural uncertainty, the description of the disturbance is well described by the vacuum. The physicist thus becomes astounded at the mutual accuracy that he observes as the number of samples measured increase. He is observing a sequence of events to greater spectral accuracy than he thinks.

The physicist who observes that time seems to dilate as objects approach the speed of light is simple observing that the vacuum is encoding the mutual entropy resulting from increased queuing as motion approaches the band limit. Thus the observed sequence has more samples available as encoding increases spectral efficiency. Fewer samples to the observed look like time dilation.

What about the person who flew around the world many times and obsverved that his clock was behind? He simply created a mutual entropy that the vacuum encoed and when he returns discovered the common component of the two clclocks has been removed and they are more different.

Newton thought the bandwidth and uncertainty was unlimited so the disturbance could be measured to any accuracy. Thus he would observe spectral separation increasing over an increasing number of samples, and invented time and distance. Spectral density of the disturbance to Newton was constant.

And Maxwell did not use the Pauli exclusion and thought waves could collisionless.

What happens when the vacuum measures everything to the ultimate limit of uncertainty? Dunno yet.

Friday, February 28, 2014

It happens in California first

Mess in the West:

Home Sales Index Hits 7-Year Low An index that measures contracts to purchase previously owned homes was mostly unchanged in January from December, according to a report Friday. But the index showed another drop in the West, where it has fallen for eight consecutive months.

The index fell in the West to its third lowest level since the NAR began its tab in 2001, surpassing only two months from the summer of 2007, when housing markets were beginning their free fall.

Western markets such as Las Vegas and Phoenix have witnessed some of the largest price gains as they rebound from very low levels. California markets, meanwhile, have grown much less affordable given the combination of price increases and higher interest rates.

The two Charles are Yellen too much

Fed’s Evans Is Willing to Risk Higher Inflation to Boost Hiring

We can start the layoffs immediately and thus avoid the hassle of repricing later on.

But Charles Plosser says we can ignore the other Charles: Fed’s Plosser: Models Hint Rates Should Rise ‘Very Soon’

Great, we can raise prices immediately and skip the lay off thing.

Then Yellen says she is ready to make a bad outlook worse:

At least she tells the truth, in her own backwards language.

Federal Reserve Bank of Chicago President Charles Evans said Friday the central bank should be willing to allow inflation to go over its 2% target if that will help the economy get back on track more quickly.

“We need to repeatedly state clearly that our 2% objective is not a ceiling for inflation,” Mr. Evans said in the text of a speech.

“A slow glide toward our goals from large imbalances risks being stymied along the way and is more likely to fail if adverse shocks hit beforehand,” the policymaker told an audience at a conference in New York held by the University of Chicago Booth School of Business. “The surest and quickest way to get to the objective is to be willing to overshoot in a manageable fashion.”

We can start the layoffs immediately and thus avoid the hassle of repricing later on.

But Charles Plosser says we can ignore the other Charles: Fed’s Plosser: Models Hint Rates Should Rise ‘Very Soon’

Many traditional models of monetary policy would suggest the U.S. central bank might need to raise interest rates quite soon, Federal Reserve Bank of Philadelphia President Charles Plosser said Friday. “Most formulations of standard, simple policy rules suggest that the federal funds rate should rise very soon–if not already,” Mr. Plosser told a conference sponsored by the University of Chicago‘s Booth School of Business. Mr. Plosser said the Fed’s communications strategy has been confusing because policy makers have made it clear they can change their minds any time. Mr. Plosser, a critic of the Fed’s bond-buying program, noted that the commitment to keep rates near zero until the jobless rate falls to at least 6.5% is no longer very useful now that the rate has already fallen to 6.6.%. “The 6.5% threshold will soon become irrelevant, and it probably is already,” he said. “Communication about the future path of asset purchases has, at times, been imprecise and confusing.”

Great, we can raise prices immediately and skip the lay off thing.

Then Yellen says she is ready to make a bad outlook worse:

A measure of U.S. corporate credit risk is heading for its biggest monthly drop since October, as the Federal Reserve reassured investors that its monetary policy remains dependent on the economy’s progress. The Markit CDX North American Investment Grade Index, a credit-default swaps benchmark used to hedge against losses or to speculate on creditworthiness, declined 8.9 basis points for the month to 62.4 basis points, after decreasing 1.2 basis points today as of 1:50 p.m. in New York, according to prices compiled by Bloomberg. That’s the steepest monthly decline since October when the gauge fell 9.1 basis points. Investors pushed the index lower this month as turmoil in emerging markets eased, consumer confidence increased and Federal Reserve Chair Janet Yellen said yesterday that if there were a “significant change” in the economic outlook, the central bank might reconsider the strategy of gradually reducing its monthly bond purchases, signaling the Fed will continue to support the economy.

At least she tells the truth, in her own backwards language.

IMF Lagarde in a panic!

IMF's Lagarde says no need to panic on Ukraine aid request

WASHINGTON, Feb 28 (Reuters) - The head of the International Monetary Fund said on Friday that there was no need to "panic" in terms of delivering economic aid to Ukraine, as she cast doubt the nation would need as much immediate help as its new leaders claim. "We do not see anything that is critical, that is worthy of panic at the moment," IMF Managing Director Christine Lagarde told reporters. "We would certainly hope that the (Ukrainian) authorities refrain from throwing lots of numbers which are really meaningless until they've been assessed properly."

But we panicked anyway.

But we panicked anyway.

Mercury News says thinking about democracy is fun

Mercury News editorial: Tim Draper's six states of California are a kick to contemplate

So, go ahead, its OK to talk about democracy. In fact, it is still legal so enjoy it. It used to be commonplace in America, you know, talking about real proportional governance. Then came the thought police of the New York Times.

The six states of California postulated by billionaire venture capitalist Tim Draper are definitely a kick to contemplate.Finally, the free spirits of the State of Jefferson, which even now proclaims its independence (if not actual existence) near the Oregon border, could go their own Wild West way, free of enviro-dictators and gun wimps. The State of Silicon Valley could dispense with a governor and make the entrepreneur king.

And those Central Valley farmers finally could -- well, what could they do about grabbing more water away from cities? Would it be easier or harder to drain the Delta if it were in another state? Would they have to declare war on the State of Silicon Valley for it? Careful, we'd have NASA.

Like the ecclesiastical debate about how many angels can dance on the head of a pin, the possibilities for a subdivided California could take up months, maybe years of evening conversations before a blazing fire (natural gas or wood), sipping a drink (Silver Oak or Coors) and spinning endless scenarios (of nanny-state utopia or free-range individualism).

So, go ahead, its OK to talk about democracy. In fact, it is still legal so enjoy it. It used to be commonplace in America, you know, talking about real proportional governance. Then came the thought police of the New York Times.

Samsung tablets suck

They want the battery always charged, even with the charger plugged in. Have they ever heard of voltage regulators? But the charger plug is so badly manufactured that the wires break if you move the tablet too much while charging. So my tablet sits, unused. I am not running out to get a third charger cable.

Thursday, February 27, 2014

This would be a change in expectations

The Bloomberg U.S. Treasury Bond Index (BUSY) rose 0.4 percent this week. It is up 0.2 percent for February, adding to January’s 1.8 percent surge that was the biggest since May 2012. Federal Reserve Chair Janet Yellen said yesterday the central bank will probably keep trimming its bond purchases, even as policy makers try to determine if recent weakness in the economy is temporary.

“Yields should go down,” said Hideo Shimomura, chief fund investor in Tokyo at Mitsubishi UFJ Asset Management Co., which oversees the equivalent of about $78.4 billion. “Growth is slowing, and it’s not temporary.”

Benchmark 10-year yields were little changed at 2.64 percent as of 9:34 a.m. in Tokyo, Bloomberg Bond Trader data show. The price of the 2.75 percent note maturing in February 2024 was 100 29/32

The Fed is tapering (easing), the economy now worries about China jitters, and 4th quarter GDP was revised, yet again, down. Tax income drops for government, but so does rates. Is this the big one? If so, count Soros as making buck on shorting the market.

Matthe O'Brien again

The Atlantic's Matthew O'Brien wants us to look at this chart.

Which supposedly shows that the bankers know more about the stock market today. And ignore the chart below which shows that bankers have been using their superior knowledge to control stock volatility.

His logic seems backwards, volatility seems larger today than in 1929. And further, the markets are getting more volatile.

If bankers and government have gotten better then why do we have this repeating pattern, and why did the market today drop much faster in 2009 than 1929? Further, is O'Brien saying that the current, nearly vertical, rise in market evaluations come from superior knowledge of today's magicians?

He claims that industrial production dropped much further in the 1929 crash. OK, but our GDP has dropped smoothly from 4% to 2% over the last thirty years. If bankers were much more accurate today, then why all the stock volatility for a mere 1/15 percent/year drop in GDP? Is he saying that the great depression was some major error in government? I don't think so, the Great Depression was a well know coordination failure, a risk well known at the time, having little to do with government.

Are time and distance real in encoder model of the vacuum?

Our model of the vacuum is that of an optimum sampler, congested by the Pauli exclusion. It is sampling the disturbance with increasing accuracy, but a bandwidth limited sample rate. In other words, a particular bit of disturbance is sampled with higher frequency quantizers, but lower frequency quantizers start measuring it also, and the order of the Huffman samples is infinite, starting with the band limit and increasingly in with slower quantizers, each quantizer having its own 'field'.

In this model, all the disturbance is undimensioned and immediate, there is no light travelling. When we 'fire' a photon, it is simply increasingly sampled in the lower modes and appears to us, with the fake variables, as moving away. It is not, the increasing dimness is simply that disturbance being captured in lower frequency modes. Black holes, galaxies, electrons are all coexistent.

Is this a consistent model? A black hole seems to have an event horizon, noticeable by us with a 15% variation. It is really light being modelled as part of an unknown, long wave length field, and the hole is just the sampler doing its normal quantization with longer wave length particles. The set of fields is infinite, energy never lost, just captured had the low frequency modes, and the disturbance being more and more accurately described. Gravity is just the next long wave length mode up, just below dark matter.

Now particles only require that the encoder be a minimum volatility sampler, particles and Pauli fall out from that.

In this model, all the disturbance is undimensioned and immediate, there is no light travelling. When we 'fire' a photon, it is simply increasingly sampled in the lower modes and appears to us, with the fake variables, as moving away. It is not, the increasing dimness is simply that disturbance being captured in lower frequency modes. Black holes, galaxies, electrons are all coexistent.

Is this a consistent model? A black hole seems to have an event horizon, noticeable by us with a 15% variation. It is really light being modelled as part of an unknown, long wave length field, and the hole is just the sampler doing its normal quantization with longer wave length particles. The set of fields is infinite, energy never lost, just captured had the low frequency modes, and the disturbance being more and more accurately described. Gravity is just the next long wave length mode up, just below dark matter.

Now particles only require that the encoder be a minimum volatility sampler, particles and Pauli fall out from that.

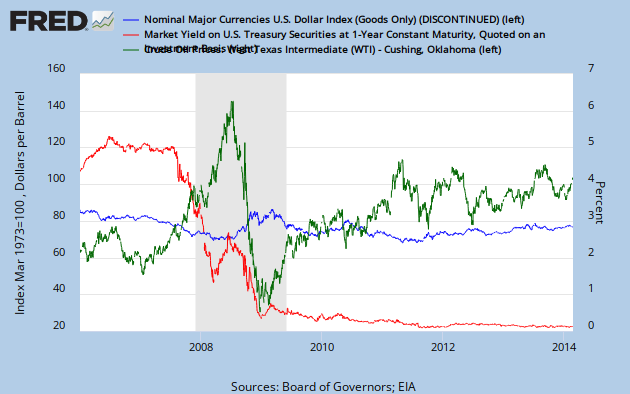

Rates too low cause price deflation, in one chart

This would be oil prices (green), Fed target rate (red) and dollar index (blue).

This would be oil prices (green), Fed target rate (red) and dollar index (blue).We see the Fed lowering the target rates in mid 2007. The return on one year reserves is too low, cash flows into deposit accounts because the return on cash is too low, and cash leaves the oil market. The economy demands more short term reserves, and will adjust cash on deposit higher if rates are too low.

But oil is still short. The market realizes this within a quarter, and raises one year rates causing oil prices to rise because the return on one year cash increase, the demand for short term cash slows and oil prices rise. Prices and rates then reflect the real shortage.

Here are the liquidity priorities: Rates barely more liquid than prices, prices a lot more liquid than oil. The more liquid thing adjusts sooner, the less liquid things adjust later. Sumner and Yglesias simply need to understand inertia and rate of change.

The trade weighted index shows that it is responding to oil shortages, not dollar rates. The dollar value rose as oil flows became stabilized. The over correction in oil prices in 2009 was likely caused by oil tankers being unable to turn on a dime. The net effect of Fed mal-adjustments was small, being easily corrected by the market within months.

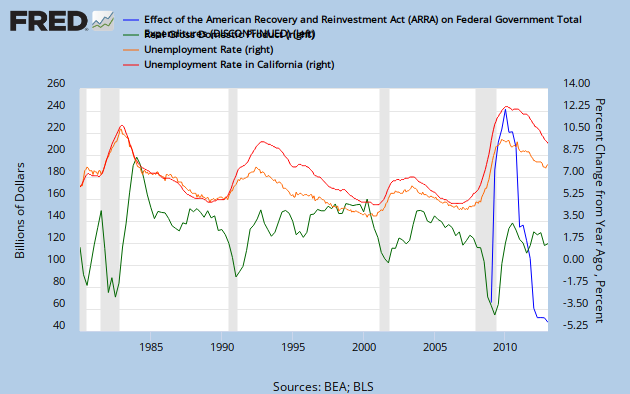

When unemployment rises the economy seeks lower velocity

That process is contractionary. The contraction was well under way before all the nuances of Fed policy were being debated in late 2008. By June of 2008, unemployment in California had jumped two points.

That process is contractionary. The contraction was well under way before all the nuances of Fed policy were being debated in late 2008. By June of 2008, unemployment in California had jumped two points.When labor gets laid off, labor conserves liquidity, it reduces short term debt and reduces velocity. Oil prices are still rising. There is nothing in Scott Sumners economic journals that can change the facts.

The stock market sees lower sales which is lower earnings and drops in stock values. What should the Fed do?

The stock market sees lower sales which is lower earnings and drops in stock values. What should the Fed do?If the economy wants to reduce velocity, then lower rates helps it do just that. If Scott wants to stop the process, then holding rates at 2% in Sept of 2008 seemed to slow the contraction, but layoffs continued.

If the economy wants lower velocity, the Fed can lead the way down, with a rate cut. If the economy wants higher velocity the Fed can lead the way up with a rate hike.

WIlliamson is correct.

Wednesday, February 26, 2014

Another "Blame the Fed" article in the Atlantic

So, what did the Fed do that was so horrible this time around that it hasn't done in any of the previous recessions? I mean, it was Clinton's eight years which broke the rule of slower growth, but otherwise this is what we would expect from an increasingly undemocratic and skewed government channel.

I did not read the Matthew O'Brien article about the minutiae of Fed decisions during the 2007 to 2009 period. Why bother. Was the Fed supposed to do something about the last 30 years of crazed government politicians?

If Matthew O'Brien thinks central banking is nuts, then say so; I happen to agree that we are no longer a sound monetary zone.

Treasuries held by the fed, all maturities

Here I have the actual mix of holdings, and the total (red) matched against the ten year yield. But the general rule still holds, whatever mix of securities held by the Fed, the ten year yield jumps as the rate of purchases increase.

Remember, in the reserve model of the economy, a five year reserve is held against the need of a firm to buy a five year machine at a random opportune moment. The firm sees the need for an additional machine, it can go to the bank and show that it has been holding 15% of the purchase price against a loan for the purchase. These liquidity reserves are fixed, and well managed by the firm. The most common depreciation schedule is likely the ten year, that is why I watch it and it seems to be the knee of the curve.

When the fed takes out the supply of treasuries, from 1 to ten, or any large interval in between, then there are fewer of the liquid reserve instruments available. To an approximation, the economy has to adjust, replacing the reserve instruments removed with a mixture of cash and ten year notes. Hence the

As a side note. When the Fed is buying the instruments Congress wants to sell, then the Fed is mismatched, in term structure, to the private sector. Its earning from treasuries held drops more than the seigniorage to Congress increases, it is a net loss to the Fed. Hence, as it supports the debt ridden Congress more, its return on holding drops, as we have seen.

So what is this tightening, loosening thing? Depends on what the target is. When the Congressional term structure is mist matched to the private sector, then the Fed has to choose. Match Congress in the near term so Congress can make the budget and tighten on the private sector or visa versa? The Fed can tighten on the private sector and make money for Congress, but maybe not in time for Congress to make its budget. But frankly, I see the financial industry as always being even in the game, able to adjust to whatever distortion the Fed creates. Congress and the Fed are stuck, in equilibrium they both go broke at the same time.

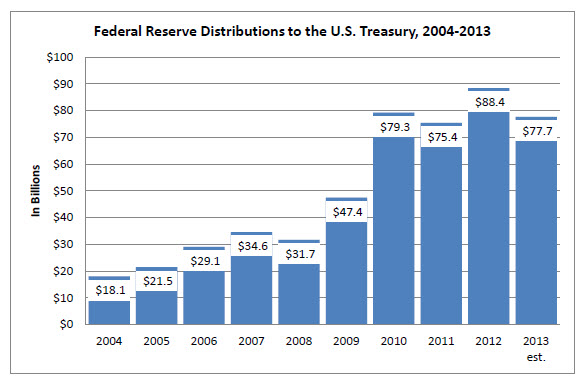

Here is the effective interest paid by Congress, and these are net returns from the Fed:

2008 32/800 = .04

2009 47/500 = .094

2010 80/800= .1

2011 75/1600 = .05

2012 88/1600 = .055

2013 78/2100 = .037

When Congress needs more seigniorage, the Fed returns drop and the effective interest drops. It looks to me that they will be simultaneously broke some time in the middle of the year. If Congress can hold on then we can delay the moment until our next regularly scheduled recession, in early 2015.

Facebook is beginning to suck

I look once a week, mainly to get e mail or other messages. The price I pay is all the damn advertising showing up and making my screen jitter.

Whew!, Just kidding

Online Content Creators Outnumber Consumers 2,000 To 1

Onion:

Given my blog popularity, I actually believed this until I saw the source.

Onion:

WASHINGTON — According to a study published Monday by the U.S. Bureau of Labor Statistics, for every person who reads, listens to, or watches some form of media on the internet, there are approximately 2,000 individuals engaged in creating new online content.

Given my blog popularity, I actually believed this until I saw the source.

A simple metaphor for the physics problem of action at a distance

The problem with quantum physics is just that it implies the vacuum is a single 16 bit computer over the vastness. A computer is a congested system, optimally designed so only one of its significant bits can change for each clock pulse. That computer cannot count the 4th bit and the 8th bit at the same time. That is also what quantum physics specifies, hence the idea that the universe is a simulation always comes up.

This is implied by my analysis, here and here. I dunno the answer, I just created the model because I know what an optimum, congested system in a bandwidth limited space should look like.

But if the speed of light is constant everywhere, one possibility is multi-processing. Light has the same speed everywhere, but its phase shifts in the vacuum sampler. In this case the vastness is a multi-processing system of identical computers. Light should have a random phase shifts.

The other possibility is that the vacuum has infinite precision but the same clock rate and same natural uncertainty. This implies that the disturbance will increasing be counted as larger and larger particles with properties yet unknown. The set of fields is infinite, but optimally separated. In this model, space disturbances slow way done, but get larger and larger. Black holes are just huge particles and fields, but unknowable by humans who live in the vacuum where disturbances are short lived and particles smaller.

Physicists need to do some more work.

This is implied by my analysis, here and here. I dunno the answer, I just created the model because I know what an optimum, congested system in a bandwidth limited space should look like.

But if the speed of light is constant everywhere, one possibility is multi-processing. Light has the same speed everywhere, but its phase shifts in the vacuum sampler. In this case the vastness is a multi-processing system of identical computers. Light should have a random phase shifts.

The other possibility is that the vacuum has infinite precision but the same clock rate and same natural uncertainty. This implies that the disturbance will increasing be counted as larger and larger particles with properties yet unknown. The set of fields is infinite, but optimally separated. In this model, space disturbances slow way done, but get larger and larger. Black holes are just huge particles and fields, but unknowable by humans who live in the vacuum where disturbances are short lived and particles smaller.

Physicists need to do some more work.

So who are these economists?

Bloomberg: Treasuries lagged behind stocks by the most in seven months on expectations the U.S. economy is growing enough to allow the Federal Reserve to end debt purchases this year.

U.S. government securities were little changed in February, based on the Bloomberg U.S. Treasury Bond Index. (BUSY) The MSCI All-Country World Index of shares gained 4.4 percent. It was the biggest difference since July. The Treasury Department is scheduled to sell $13 billion of two-year floating-rate debt and $35 billion of five-year fixed-rate notes today.

“The equity markets will rise because of the good shape of the U.S. economy,” said Hiroki Shimazu, the senior market economist in Tokyo at SMBC Nikko Securities Inc. The company is a unit of the nation’s second-biggest bank by market value. “The U.S. Treasury yield will also rise because of the good shape of the economy.”

Benchmark 10-year yields were little changed at 2.71 percent as of 1:08 p.m. Tokyo, Bloomberg Bond Trader data show. The price of the 2.75 percent note maturing in February 2024 was 100 10/32.

The yield will be 3.37 percent by year-end, based on a Bloomberg survey of economists, with the most recent forecasts given the heaviest weightings. The move would hand a 2.8 percent loss to an investor who buys today, data compiled by Bloomberg show.

The ten year rate will rise because ten year depreciated machines like trucks, lathes, and houses will be moving thru the economy. Is that true?

Housing starts, slightly up over the year.

NEW YORK, Jan 28 (Reuters) - U.S. Treasuries prices edged up on Tuesday after data showing an unexpected fall in orders for U.S. durable goods in December spurred safe-haven bids, but nervousness ahead of the Federal Reserve's policy decision capped gains.

The Commerce Department reported that orders for long-lasting U.S. manufactured goods fell by 4.3 percent in December.

"It does paint a much bleaker picture for the U.S.," said Aaron Kohli, interest rate strategist at BNP Paribas in New York.

Home purchase applications:

Home sales are slow, but that is not a lot of volatility, not a killer crash.

Otherwise, corporate profits conue up, but half of that up is outside of the US.

Conclusion: The private sector is a slowing a bit, but it is not going to crash. These economists will eat a bit of crow. The government in DC is due to crash sometime in the next two years, however. It is a regularly scheduled crash.

Say's Law and financial bankruptcy

The issue is, simply, did bankrupt brokers get a bad deal because they had to sell assets in a rapidly declining market?

If hold the mortgage on a house then the owner goes bankrupt, I take ownership of the house. What I lost was the transaction cost of the bankruptcy. The house remains empty for a period until I can rent or sell it. I suffered from holding an illiquid asset for some period, but then it was reconverted into a liquid asset once again.

Was total liquidity lost in the economy after the crash? No, but transaction costs going down hill increased relative to going up hill. If the economy did the dead cat, then unnecessary transactions took place, that is a loss. Aside from those efficiency costs, we ended up with a slower economy, velocity was reduced so money changes hands less often. Hence, there are fewer piles of liquidity, and each pile is bigger. Velocity has slowed, and more processing and value added is done within fewer firms or households rather than hired out.

Presumably the economy did this to reduce total costs because the previous state of affairs contained severe inventory shortages. In fact, my claim is that if this contraction was planned well, then it would be neutral to relative prices, except that pricing would have courser quantization.

Was there some destruction of inventory? Not much, but I saw a few half finished houses being torn down. The economy chose to increase its reserve ratio from 9% to 15%. It paused momentarily at 11% because of delusions among the bankers which caused unnecessary volatility. But the economy then then proceeded on its journey to 15% with alacrity.

What about winners and losers? The economy has winners and losers all the time. In a rapid contraction they show up in bigger crowds.

If hold the mortgage on a house then the owner goes bankrupt, I take ownership of the house. What I lost was the transaction cost of the bankruptcy. The house remains empty for a period until I can rent or sell it. I suffered from holding an illiquid asset for some period, but then it was reconverted into a liquid asset once again.

Was total liquidity lost in the economy after the crash? No, but transaction costs going down hill increased relative to going up hill. If the economy did the dead cat, then unnecessary transactions took place, that is a loss. Aside from those efficiency costs, we ended up with a slower economy, velocity was reduced so money changes hands less often. Hence, there are fewer piles of liquidity, and each pile is bigger. Velocity has slowed, and more processing and value added is done within fewer firms or households rather than hired out.

Presumably the economy did this to reduce total costs because the previous state of affairs contained severe inventory shortages. In fact, my claim is that if this contraction was planned well, then it would be neutral to relative prices, except that pricing would have courser quantization.

Was there some destruction of inventory? Not much, but I saw a few half finished houses being torn down. The economy chose to increase its reserve ratio from 9% to 15%. It paused momentarily at 11% because of delusions among the bankers which caused unnecessary volatility. But the economy then then proceeded on its journey to 15% with alacrity.

What about winners and losers? The economy has winners and losers all the time. In a rapid contraction they show up in bigger crowds.

Tuesday, February 25, 2014

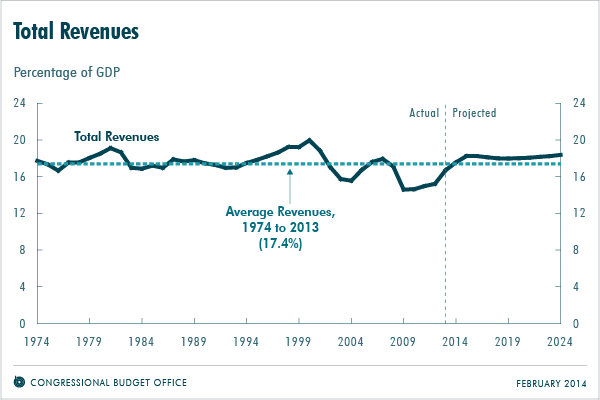

The CBO is humorous

Federal Revenues Are Projected to Increase Significantly Over the Next Two Years and Remain Steady as a Share of GDP Thereafter

Says the CBO

Actually not. Federal revenues are expected to cycle along with the presidential elections, a period of 8 years. Looks like they are going to cycle downward right along with the elections this year, a bit early maybe.

The CBO method of analysis is 'Kick the Can'

I also predict the Fed return on debt will continue dropping while Congress drains the spigot. That would mean sometime in a few months, Congress will be cut off.

Vacuum as a sample space

If the speed of light is constant, and the uncertainty natural, then a vacuum, as a Huffman encoder, then a vacuum has already determined all the fields available, and their relationships. This all results from the Pauli principle and a finite bandwidth system transmitting the most information with the least congestion. Sort of weird, but who knows?

Congressional net return from the Federal Reserve

2008 32/800 = .04

2009 47/500 = .094

2010 80/800= .1

2011 75/1600 = .05

2012 88/1600 = .055

2013 78/2100 = .037

Jared Berenstein is still fraudently wrong

Jared: It was five years ago this month that the new president signed the $800 billion Keynesian stimulus package, also known as the Recovery Act. A few weeks later, he put Vice President Joseph R. Biden Jr. in charge of overseeing its implementation. As the vice president’s chief economist at the time, as well as a member of the economics team that helped to shape the package, I was an active participant in this important chapter of our economic history.

He imposes his priors. His implied claim is that the increase in debt to gdp from 2008 to 2014 was nmainly because we didn't increase it fast enough from 2008 to 2011, the stimulus. In other words, most of the additional debt to gdp was due to a failure of government to fix the economy. Bill McBride, of calculated Risk, praises that view, mainly because he is can't do the math.

The distinction between debt raised by Congress and called stimulus and debt raised by Congress and called something else is plain BS, a prior belief mainly used to cover up really bad multipliers. The stimulus was $800 out of a 16 trillion dollar economy, about 5% of GDP. The economy rose about 10% during the period. But total additional spending above baseline debt to GDP was about 50%. So Jared wants to say the the total rise in debt was mostly economic error, but the stimulus portion of that was a corrective adjustment.

What corrective adjustment was that exactly? Shovel ready projects that were previously unfunded. But that is true of the entire 50% increase in debt to gdp during the period. It was all shovel ready projects that were unfunded, in fact, it was almost all the previously unfunded government plans. Unfunded mainly because the broken economy could not afford them. So what did DC do? DC took all the unfunded projects from 2008 until 2013 and funded them with new debt.

How is the one different than the other? The total stimulus was everything unfunded in 2008 but now funded with debt in 2013, and that multiplier is low, about .25. Jared has no basis for calling some of it stimulus and some of it normal debt.

Government destroyed my reputation?

Zero Hedge: In the annals of internet conspiracy theories, none is more pervasive than the one speculating paid government plants infiltrate websites, social network sites, and comment sections with an intent to sow discord, troll, and generally manipulate, deceive and destroy reputations. Guess what: it was all true.

And I thought I did it to myself all this time!

Monday, February 24, 2014

Federal debt multipliers yet again

We have the increase in federal debt to nominal gdp (red) and the increase in nominal gdp (blue). The change in GDP was 16 points during the period from 2008 to June 2013, The total nominal GDP increased by 16 index points.

The change in debt to GDP was 60 index points, so the economy changed 16 index points to the government 60. The government spending changed 60 from a starting point of 100, the total economy changed 16 from the starting point. A multiplier of 16/60 says each increase in government spending associates with an increase in total spending of .26.

If DC were balanced, then the private sector and DC should grow together, by the same percentage. That is, both DC and the private sector should be responding equally to the external shock, positive or negative.

Nyquist, Pauli and reserves

C/B = log_2 ( 1+SNR)

where C is the channel capacity in bits per second; B is the bandwidth of the channel in hertz (passband bandwidth in case of a modulated signal); S is the average received signal power over the bandwidth (in case of a modulated signal, often denoted C, i.e. modulated carrier), measured in watts (or volts squared); N is the average noise or interference power over the bandwidth, measured in watts (or volts squared); and the signal-to-noise ratio (SNR) .

So lets assume the firm or household want to know the most it can the soonest, then the economy samples C at twice the bandwidth, or C/B = 1/2. (2**1/2)-1 = SNR = .4. But that number is split in a queuing network, the sender gets .2 the receiver gets 2. Add in congestion and the number goes to .15, or thereabouts. Real scientists can get the right number, but it is a constant. It is determined by the need to get the most information with the best transaction rate.

So for physicists, assume the particle and you get the natural uncertainty.

where C is the channel capacity in bits per second; B is the bandwidth of the channel in hertz (passband bandwidth in case of a modulated signal); S is the average received signal power over the bandwidth (in case of a modulated signal, often denoted C, i.e. modulated carrier), measured in watts (or volts squared); N is the average noise or interference power over the bandwidth, measured in watts (or volts squared); and the signal-to-noise ratio (SNR) .

So lets assume the firm or household want to know the most it can the soonest, then the economy samples C at twice the bandwidth, or C/B = 1/2. (2**1/2)-1 = SNR = .4. But that number is split in a queuing network, the sender gets .2 the receiver gets 2. Add in congestion and the number goes to .15, or thereabouts. Real scientists can get the right number, but it is a constant. It is determined by the need to get the most information with the best transaction rate.

So for physicists, assume the particle and you get the natural uncertainty.

Estimate recession risk with the presidential cycle

Estimating Recession Risk With Potential GDP

Will the period be shorter this year? Good question. This regularity is the secstags, and it is increasingly priced in. So the more often that investors look at this chart, and have a clue, the more often they set aside reserves for the recession. That causes a smooth down turn. So watch growth this year. If we keep it near or below 2%, then investors and state governments have the secstags priced in.

Watch Cynthia Wu's shadow policy rate, if that gets lower and lower then the secstags are not being priced in. The stock market is way up today, so the short shadow rate has dropped, as seen by the brokers. Stocks are shifted into short term liquidity reserves, mainly being moved away from ten year liquidity. Fewer stocks held for ten years and more held for one year. The ten year rate is up, there are fewer ten year reserves today than yesterday. A steeper curve. Thus fewer reserves held against ten year events, like presidential cycles. Today we have discounted the secstags, tomorrow we will price them back in.

Saturday, February 22, 2014

Why our brains do it

As a Huffman encoder, look at the encoding graph. That is the minimal graph needed to encode sequences, the minimal number of nerve impulses, because we are sub-machine, we only have five of six quantization levels. The the nerve firing is still there, the overlapped, mutually entropic, firing graphs to measure the world to a five bit accuracy. But look at the frequency range, 30 years. So we have encoded the environment with low frequency pre encoded symbols, like national monuments and bill boards. These are also, Shannon encoded around our environment. Every thing we know is Shannon encoded, some where. If externally triggered, say by a magazine about the Beatles, we trigger the 'I dig classic' sequence, which are optimum actions, or firings, to try for the big quant, the firings that generate some pop music, especially a good concert.

Going to a public event, a set off brain firings that take you through those actions, phased with external cues from the external event organizers.

So, apply the Nyquist principle to politics, namely encoding the government channel. Here in California we measure a four deep channel, the small state a three deep. That is skew, it appear at a leaning to one side Huffman graph. A temporary quantum limit, so we encode local operators, to sample nearly twice as fast as the voters, and make the channel balanced. These would be party hacks.

Our brains do not like skewed government, this is biology and culture; a result of our big bang. If government does not encode for balance, the Says Law violation thing is built in. We have many cultural symbols, all Shannon encoded, and all Say's Law violations. They are sprayed about our environment. They get triggered.

Anyway. The great utility of human innovation is leaving external cues in the environment, like stock bets, art, religion, meetings, or machines and companies. They are cues that trigger sequences, cues that are Shannon encoded.

The great fun of forensic science is to decode external cues, with the original sequence. We are dominantly decoding with birth and childhood sequence, making some strongly compelled emotionsl firing sequences. Anxiety is when the deep sequence is triggered, but are not in mutual entropy with current sequences, or environment. So in the brain we should find depleted neurotransmitter during periods when deep sequences are triggered. The sub conscious and suppression is likely a neuro transmitted rebalance. Traumatic experiences ate reactions, neural firings, which have excess neuro-transmitter, the reaction is easily triggered.

This model suggests suppression and self identification are neurons that modify neuro transmitter levels in deep reactions. We are conscious because we can self medicate parts of the brain.

Going to a public event, a set off brain firings that take you through those actions, phased with external cues from the external event organizers.

So, apply the Nyquist principle to politics, namely encoding the government channel. Here in California we measure a four deep channel, the small state a three deep. That is skew, it appear at a leaning to one side Huffman graph. A temporary quantum limit, so we encode local operators, to sample nearly twice as fast as the voters, and make the channel balanced. These would be party hacks.

Our brains do not like skewed government, this is biology and culture; a result of our big bang. If government does not encode for balance, the Says Law violation thing is built in. We have many cultural symbols, all Shannon encoded, and all Say's Law violations. They are sprayed about our environment. They get triggered.

Anyway. The great utility of human innovation is leaving external cues in the environment, like stock bets, art, religion, meetings, or machines and companies. They are cues that trigger sequences, cues that are Shannon encoded.

The great fun of forensic science is to decode external cues, with the original sequence. We are dominantly decoding with birth and childhood sequence, making some strongly compelled emotionsl firing sequences. Anxiety is when the deep sequence is triggered, but are not in mutual entropy with current sequences, or environment. So in the brain we should find depleted neurotransmitter during periods when deep sequences are triggered. The sub conscious and suppression is likely a neuro transmitted rebalance. Traumatic experiences ate reactions, neural firings, which have excess neuro-transmitter, the reaction is easily triggered.

This model suggests suppression and self identification are neurons that modify neuro transmitter levels in deep reactions. We are conscious because we can self medicate parts of the brain.

How the Fed loses money to Treasury curve betters

NYT: Because the Fed mostly holds debt issued by the federal government, its profits — which totaled $91 billion in 2012 — are largely payments from the government. By returning that money to the government, the central bank in effect is letting the government borrow at no cost.

Earnings in the sense the Congressional seigniorage are profits from owning the fed. These are Jan 2013 numbers and the Fed held about 1.7 trillion in debt, at the time. The $91 billion comes from 1.7 trillion held by the Fed. Assuming the securities held by the Fed are liquid reserves, then the Fed, and government, earns about 5.0% on its reserves. The economy earns about 2.3% on its reserves, the growth rate optimally invested in liquid markets. Reserves are about 15% of operational flow, so the Fed is ill matched, having 50% of the reserves it needs to match the economy, or 8% reserves. The Fed moves twice as slow.

The economy, at equilibrium, will always generate a 15% variation in GDP growth, or a 15% variation in the real yield curve. Fed operations will always generate an 8% variation in the Treasury curve. The difference, 7%, is the Fed induced delays in Treasury curve, the error between what the Fed thinks and what is real. That is free money to Soros and the Treasury curve betters. Well, 17 trillion are rolled over in the Treasury curve, and the rates on that about 4% in real terms, so Soros Treasury curve betters can earn .04 * 17 Trillion * .07, or 4 billion a year.

Reserves and accuracy in the model.

Reserves are a very well measured, liquid Gaussian noise single that the firm intends to impose on cash flow. The firm knows the variation in inventory to high accuracy, and knows the reserve variation to high accuracy. Thety are well matched and equally uncertain. The high accuracy of measuring reserves comes from liquidity, which varies by less than 3%. The high accuracy of measuring inventory flow is from the firm using a Huffman encoder over the sequence, in the past, or known arrivals. The equivalence between liquidity and accuracy is from the transaction rate, high, it sits way left on the yield curve of goods. The liquid good still imposes its own 15% variation on GDP changes, but it counts in much higher quantization levels, it carries more types of -log(i) So, real goods sticky because they impose a bandwidth limit on themselves. So, you see, Soros and government agree, government imposes a 8% volatility, and Soros has a 15%. Soros counts twice as fast as government, to within a 3% accuracy. He is the first to reverse engineer the Fed, his reaction time, two quarter, aha, there is Nyquist. Soros gets the most accurate measurement the soonest.

We can define the Plank limit. It is twice the bandwidth, (left on the curve) between liquidity times -1/2*log(1/2). Or so, don't quote me. But that is he next -ilog(i) down the curve. Twice that quantum limit is your best liquid thing, at equilibrium.

The issue here is why the 15%? That is Pauli exclusion. The any Gaussian decompose to the Nyquist. Take the Bell, divide it in half, take a sigma chunk, your have two delivering containers. The tails get you a reserve. Nyquist applies, it is fundamental to minimizing transactions. So that number is the SNR in the Shannon equation. The firm is taking entries, which deliberately share 15% of the roadways. The bandwidth is at the other side. Well covered with liquidity, then, the real issue is the bandwidth between the liquid thing and the illiquid. Hence the drive for faster money, faster trades, the firm wants to encode with more symbol capability then the illiquid which measure bigger things. The key is well covered, like a smart card that can mange many currency contracts.

The rule then, in retail, is no more than two in a line. 1.65, no problem. That means the, at just below Nyquist, 1.65 customers in line then the clerk gets sampled the mostest That is nearly the Nyquist, optimum. Nyquist and Pauli can be viewed as the optimum sampler.

A fun Zero Hedge chart

Zero Hedge has a bunch of charts, all them all here.

Zero Hedge has a bunch of charts, all them all here.Here we see the Fed is holding potential inflation and the market is adjusting total return to compensate. If the Fed sold its holdings into the market, its prices would be steeply discounted. That sterilizes the seigniorage granted to Treasury, the seigniorage becomes loose inflationary cash.

Government, which is a money loser, will either go broke and the inflation released, or government will restructure and the Fed assets held become a wise investment. That is why we are wise to restructure government, to turn this investment into a gain, not a loss.

That's a fine mess you got yourself into, Mr. Putin

Ukraine crisis: Opposition asserts authority in Kiev

BBC:

Ukraine's opposition has asserted its authority over Kiev and parliament in a day of fast-paced events. MPs have replace the parliamentary speaker and attorney general, appointed a new pro-opposition interior minister and voted to free jailed opposition leader Yulia Tymoshenko. Police appear to have abandoned their posts across the capital. Protesters in Kiev have walked unchallenged into the president's official and residential buildings. President Viktor Yanukovych and opposition leaders signed a peace deal on Friday after several days of violence in which dozens of people died in a police crackdown on months of protest.

The message here is simple, politicians should learn how information flows before engaging in deceit. Our politicians will learn this fairly fast as the rebels continue to close in on the USA.

Speaking of information flow, let us see the latest results from Tim Draper's idea.

Here is a poll, split three ways. No, yes but not so many states, and yes. Let us divide them into, yes, some sort of split and no, not at all. So the yes, some split is 40%, no not at all is 58%. This is up from 23% vs 65% a few months ago. This is called the flow of information, voters figuring out that democracy is really important. Voters are pricing in the secstags, and politicians, as usual, are as dumb as Putin at the moment. Politicians will get on this pretty quick. My own rep, Jim Costa in Fresno, Ca, may progress from incredibly stupid to just a bit less stupid; which would be a miracle.

That would be inflation swining wildly down, professor Krugman

Says the Professor:

Says the Professor:

What’s kind of shocking about this is that official Fed doctrine is to focus on core inflation, not react to short-run fluctuations in commodity prices. And the history of the past decade or so has showed that this is very much the right thing to do — headline inflation has swung widely, while focusing on core inflation has been a much better (though not perfect) guide to appropriate policy.

What is his point? We have a disinflationary trend over the last thirty and the ten year bond has been dropping right along. The ten year has been continuing to drop, to negative rates as we see here.

What is the outcome? Money markets abandon the low income consumer and serve only the wealthy. The low end consumer, without the utility of money, rebels. The result should be a better formed democracy, or alternatively, the result could be Venezuela. I think the former. I think the rich who are well served by Krugman philosophy will realize that the only hope is a fair democracy, like the one Tim Draper is proposing.

Friday, February 21, 2014

Taking on Krugman once more

Governments in structural balance have no problem changing their deficit in response to interest rates hikes. Government in balance still have taxable reserves. So Krugman needs to change the X axis to stimulus, getting smaller to the right. Krugman is really saying that countries to the right should be stimulated by countries to the left, he just tries to hide the fact.

Stimulate, in this case, means to ease their path downhill.

That would be socialists shooting citizens

The US has a better idea:

Plan to split California into six states gains ground

Los Angeles (United States) (AFP) - A plan to divide California into six separate US states is closer to making it on to a November ballot, with organizers gaining approval to collect signatures. The seemingly far-fetched initiative, sponsored by Silicon Valley venture capitalist Tim Draper, claims "political representation of California's diverse population and economies has rendered the state nearly ungovernable."

Wages are sticky?

Thursday, February 20, 2014

Uncle Milt's Error

When the consumer is in balance, reserves cover the arrival variation of goods, the error in pricing and the return on reserves. So the bank lowers rates below that level. The consumer will save more, borrow less and suppress prices until the return on reserves again balances.

The effect on the bank is that they have to be much more efficient, more efficient then they think. Inflation is not generally a bank error.

The effect on the bank is that they have to be much more efficient, more efficient then they think. Inflation is not generally a bank error.

Productivity and roundaboutness

What happens when we got a huge productivity shock like electricity to the home? We got a great variety of home appliances powered by electricity. This is a rebalacing of distribution, and should be price neutral. The electricity network thus grows in depth and breadth, and the flowering of new products is the distribution rebalancing by taking advantage of a cheap new resource.

The problem we have with tech titans today is their control of the software chain and they bundle the new applications. The counter force are new tech start ups trying to build breadth, or unbundle the applications.

The secstags are the result of government no longer able to deliver a breadth of applications because the mall/large state gap is to expensive to DC to bridge. That gap is getting worse.

The problem we have with tech titans today is their control of the software chain and they bundle the new applications. The counter force are new tech start ups trying to build breadth, or unbundle the applications.

The secstags are the result of government no longer able to deliver a breadth of applications because the mall/large state gap is to expensive to DC to bridge. That gap is getting worse.

How times have changed

Yahoo: “It’s not too late” for Apple to make a move at this point, Najarian says. Indeed, rumors of Apple kicking the tires on Tesla (TSLA) had many investors, and Apple fanboys, giddy for such a merger. But Apple has to do something real, “they have to make moves in social,” Najarian notes, “otherwise they become Microsoft (MSFT).”

A few years ago that statement had the opposite sign, people feared Apple could not be the next microsoft.

Have physicists proved that the uncertainty constant is the same everywhere?

This seems to bee a relevant issue regarding cosmology, do we have an answer?

Irrelevant information is not well maintained

Peter Gordon:

Head scratchers

Accuracy is a limited quantity. We use it only for transactions that count. Ask me something I am not really concerned about, I will make stuff up just to keep you happy.

We suspect that many people are not well informed. Why should they not believe that wages can be set by edict and that there are no consequences? Why not believe in free lunches? This study suggests that widespread ignorance is even worse than we suspect.

Accuracy is a limited quantity. We use it only for transactions that count. Ask me something I am not really concerned about, I will make stuff up just to keep you happy.

Finding microsecond uncertainty levels

From Nanex:

Here Is How High Frequency Trading Hurts Everyone

Market traders are increasingly using web bots to measure information levels in the market. The rule is simple. If you put a quote on the market that is a level change greater then the market can measure, then you reveal information which is value. But the more value you release, the faster your trade converges. As the web bots become increasing certain, the trades have to be broken up to match the Shannon model of information flow, but the sample rate, or event rate becomes a million per second. The certainty of the human remains the same, but that certainty is broken into ever smaller chunks by the bots. The problem that Nanex points out is that many humans still do not have a Huffman encoder managing their trades, and they get discouraged. The solution is for traders to hire a high school kid and code up the algorithm I just linked to.

The market value of a stock quote continues to plummet. As Nanex shows so graphically below, it's taking more quotes to get the same amount of trading done in today's stock market, meaning that everyone has to process more information than ever before, yet actual trading continues to stagnate.

Market traders are increasingly using web bots to measure information levels in the market. The rule is simple. If you put a quote on the market that is a level change greater then the market can measure, then you reveal information which is value. But the more value you release, the faster your trade converges. As the web bots become increasing certain, the trades have to be broken up to match the Shannon model of information flow, but the sample rate, or event rate becomes a million per second. The certainty of the human remains the same, but that certainty is broken into ever smaller chunks by the bots. The problem that Nanex points out is that many humans still do not have a Huffman encoder managing their trades, and they get discouraged. The solution is for traders to hire a high school kid and code up the algorithm I just linked to.

Putin should think more and masterbate less.

WA Post: KIEV, Ukraine — Ukrainian President Viktor Yanukovych has told European foreign ministers that he is open to early presidential and parliamentary elections as a way of resolving Ukraine’s deepening and increasingly violent crisis, the Polish prime minister said Thursday evening in Warsaw, according to news services.

Yanukovych met with the top diplomats of Poland, France and Germany for four hours in the afternoon, after which his visitors left to confer with opposition leaders.

Radislaw Sikorski, of Poland, tweeted that they went to “test a proposed agreement” with the heads of the three main political parties opposing Yanukovych. Afterward, as it grew late, the three returned to the presidential offices and met with Yanukovych again.

Thinking things thru causes less coordination failure.

Wednesday, February 19, 2014

The reserve system using Shannon Theory

Assume the firm that has a five year machine and replaces it every five year, plus or minus 3/4 of a year. The arrival of the next machine can vary by 15%. The firm balances income and expenses to buy the machine but must hold 15% of the cost in liquid reserves, available on a moments notice when the next machine arrives. If money were perfectly accurate, then the firm loses no opportunity cost, the yield curve is flat.

But money itself varies. The price of money is set every 1/4 of a year and the price of five year machines is set every five years, to accuracy. The yield curve is generally drawn for liquidity, not five year machines. It is the bankers curve.

The price variation in the price of a five year machine is the five year interest rate. How do we compute that interest rate? We have to assume pricing is measered ten years, or 40 pricing events.

The variation on 1/4 year money is -(1/4)log(1/4)

The variation on five year money is -(1/10)log(1/10)

The negative log value is the interest rate,y the cucrve is drawn as -log(1/4) -log(1/7) etc. and the X axis is the relative arrive rate.

These are set in a congested system that is balanced so the inventory of both five year prices and one year prices have the same variation, the two values above must be within an integer of each other.

Machines also have the same relationship, in a value added network, the Shannon system maximize the mutual entropy between money and machines. Whether money, or machine; whether one year of five year, the probability that an inventory runs out is the same. Run the same curve pn a valie added net makong pne year machines. The -log value is then the relative price of any machine measured in units of machine.

Machines do not completely populate the curve, they are illiquid. But, at equilibrium, the machine curve, written to the nearest polynomial is a factor of the money curve.

The short hand way to handle this is with accuracy, machines have about an 8% accuracy relative to the accuracy of money, which is closer to 3%. The difference in accuracy is the length of the value added, congested networks that deliver them. Money is fast, machines are slow. But the slow network should fit into the fast network at equilibrium when mutual entropy is maximized.

But money itself varies. The price of money is set every 1/4 of a year and the price of five year machines is set every five years, to accuracy. The yield curve is generally drawn for liquidity, not five year machines. It is the bankers curve.

The price variation in the price of a five year machine is the five year interest rate. How do we compute that interest rate? We have to assume pricing is measered ten years, or 40 pricing events.

The variation on 1/4 year money is -(1/4)log(1/4)

The variation on five year money is -(1/10)log(1/10)

The negative log value is the interest rate,y the cucrve is drawn as -log(1/4) -log(1/7) etc. and the X axis is the relative arrive rate.

These are set in a congested system that is balanced so the inventory of both five year prices and one year prices have the same variation, the two values above must be within an integer of each other.

Machines also have the same relationship, in a value added network, the Shannon system maximize the mutual entropy between money and machines. Whether money, or machine; whether one year of five year, the probability that an inventory runs out is the same. Run the same curve pn a valie added net makong pne year machines. The -log value is then the relative price of any machine measured in units of machine.

Machines do not completely populate the curve, they are illiquid. But, at equilibrium, the machine curve, written to the nearest polynomial is a factor of the money curve.

The short hand way to handle this is with accuracy, machines have about an 8% accuracy relative to the accuracy of money, which is closer to 3%. The difference in accuracy is the length of the value added, congested networks that deliver them. Money is fast, machines are slow. But the slow network should fit into the fast network at equilibrium when mutual entropy is maximized.

Lost productivity should appear in diversity

If we believe that our reserve ratio is constant, then increased productivity shows up in diversity. Why are we not a more diverse society? We make Florida into a specialized retirement state, under serve the small states, agglomerate the large states of Texas and California. Why do we always seek guarantees and insurance in DC? Productivity has not reached our political system. The western states needs to assert itself, the small states find better methods of agglomeration

Holding less cash and relying on more transfer payments

This is hiding volatility from the labor, and that is a bad thing. Volatility is a useful signal, and DC is an erratic signal passer.

I puzzled over this until I remembered Kling's post. Liberals do not get the problem, and they inevitably leave poor people stranded and the wealthy end up with the money.

So, you take this sunbelt state like Florida which lives on government transfers and bubbles. The volatility of federal government comes, on schedule each presidential cycle, and Florida is cut short, no cash reserves. Unemployment shoots up. Same in California.

This is a malformed democracy which cannot transmit signals. On the one hand you have Mankiw completely clueless about masking volatility thru federal support of monopolies, and opposite we have Krugman masking volatility by supporting transfers. Both of them clueless.

But these small states control the Senate, and they are under deflationary pressure. They normally rely on discretionary spending by the Senate and do not have the economies of scale to manage. Hence the inevitable political restructuring. DC cannot support both without massive fraud, and DC is uncovered, the undemocratic beast that it is.

Tuesday, February 18, 2014

Having fun with Steve Williamson's production curves.

Here is what's called the production frontier graph. The Y axis tells us how much consumption goods are produced and the X axis tells us how much time off from work we have. If we want more consumption goods we have to give up time at home and spend more time on the job. The two lines called PPF1 and PPF2 are the production frontier curves, they are drawn by the boss. The Boss says if you want more time at home you get less consumption goods. So, each of those curves slopes down, more time at home fewer consumption goods. There are two lines because Steve assumes something went wrong at the factory, a machine broke and the boss drew a new curve. Before the machine broke we had PPF1 curve, after the machine broke we have PPF2 curve. When the machine breaks it takes more time on the job to get the same consumption goods.

Here is what's called the production frontier graph. The Y axis tells us how much consumption goods are produced and the X axis tells us how much time off from work we have. If we want more consumption goods we have to give up time at home and spend more time on the job. The two lines called PPF1 and PPF2 are the production frontier curves, they are drawn by the boss. The Boss says if you want more time at home you get less consumption goods. So, each of those curves slopes down, more time at home fewer consumption goods. There are two lines because Steve assumes something went wrong at the factory, a machine broke and the boss drew a new curve. Before the machine broke we had PPF1 curve, after the machine broke we have PPF2 curve. When the machine breaks it takes more time on the job to get the same consumption goods.Since we have proof positive the government is the thing with the broken machines, we can see what happens to the government production curve. Government breaks on of its machines about every eight years, on the presidential cycle when we have a recession. That is why real growth has been dropping for 30 years. We are now at PPF5, which is not shown, but it is a production curve way down in the corner where the X and Y axis meet. We simply do not have any more free time left if we try and obtain any government goods, that is Zero Bound.

So what happens? Well, we all know the problem and government cannot break beyond the zero bound. So we get an orderly restructuring of government, and we have many options within the Constitution to do this. Government in DC cooperates because they are the first to know that government is in need of restructuring.

Now what is this error that I keep talking about with respect to the real business cycle? Simple, the Boss does not redraw the curve all at once. We all notice the goofs as they come and we adjust the curve as the goofs are observed. Hence with the greater incremental knowledge, we price in the cost of restructuring as we go. Finally when the event happens, we have the restructuring schedule computed as we go and keep reserves against the errors of government. We include the cost of restructuring in the production curve as we go down hill. The accumulated cost of restructuring is called the government debt, and the super wealthy keep that same percentage of reserves to cover government inefficiency.

Gail Finney, Dem from Kansas want us to beat our children

How to beat the crap out of children. She describes the method of abuse, wants it part of the law.

Ryan Avent takes on the secstags

Here.

I summarize. The secstags are a failure of labor to keep up with technology.

Says Ryan.But where to the recessions come from? Government, they happen on presidential election cycles. Why does government play a substantial role in causing this problem? Mainly because the US government suffers severe over aggregation. Government grants monopolies on over the wide economy while hiding the volatility from labor. The data will bear me out. Mankiw misses this because he believes undemocratic government should support monopoly producers. Larry Summers misses this because he teaches government fraud at the Harvard School of Government Fraud.Krugman misses this because he thinks government should hide volatility from labor. DeLong and Reich miss this because they teach at the UC Berkeley School of Government Fraud. Prescott misses this because of a statistical mistake. Kling misses this because he he thinks disequilibrium is an unbound quantity. The Austrians miss this because they do not know how to compute roundaboutness. Monetarists miss this because they do not use a stock and flow model. Keynes makes the same statistical mistake that the RBC folks make.

I summarize. The secstags are a failure of labor to keep up with technology.

Mark Bils, Yongsung Chang, and Sun-Bin Kim find that sticky wages push firms to wring more output from existing employees when confronted by a decline in demand. Productivity therefore rises during recessions—rising most in industries where wage rigidity is most binding—reducing the incentive to take on new workers despite relative wage flexibility among the unemployed.

Says Ryan.But where to the recessions come from? Government, they happen on presidential election cycles. Why does government play a substantial role in causing this problem? Mainly because the US government suffers severe over aggregation. Government grants monopolies on over the wide economy while hiding the volatility from labor. The data will bear me out. Mankiw misses this because he believes undemocratic government should support monopoly producers. Larry Summers misses this because he teaches government fraud at the Harvard School of Government Fraud.Krugman misses this because he thinks government should hide volatility from labor. DeLong and Reich miss this because they teach at the UC Berkeley School of Government Fraud. Prescott misses this because of a statistical mistake. Kling misses this because he he thinks disequilibrium is an unbound quantity. The Austrians miss this because they do not know how to compute roundaboutness. Monetarists miss this because they do not use a stock and flow model. Keynes makes the same statistical mistake that the RBC folks make.

John Taylor is half right on the stimulus

John Taylor: As a whole the findings summarized here provide evidence that the stimulus was not successful in jump-starting the economy or in stimulating sustained growth. Similar results were found in stimulus packages in the 1970s. Keeping a record may help us remember the lessons so we don’t do it again next time.

He gets the obvious point he made many times, the stimulus mostly offset state spending. He misses the point I have just made, the stimulus prevented the dead cat bounce we see in the 81 recession. Why no dead cat bounce? Mainly because that money sent to the states was money previously expected from the Feds, but fraudulently stolen by the Bush administration.Reagan got a dead cat bounce because our knowledge of the secstags, caused by an ill government channel, were just being learned.

Monday, February 17, 2014

Krugman and the stimulus

Then we have Krugman explaining the error in the real business cycle.

Take real business cycle theory – I know it’s a horse I beat a lot, but it’s not dead, and it’s a prime example within economics of what I have in mind. I still want to spend at least some time explaining that theory to my undergrads, so I’ve been looking for a simple, intuitive explanation by an RBC theorist of what’s going on. And I haven’t been able to find one!I mean, I could do it myself. Strip the story down to basics – make it a steady-state model, not a growth model, and drop the capital accumulation; what you’re left with is fluctuations in the marginal productivity of labor, which have a magnified impact on output because workers choose to work less when the technology is bad and more when the technology is good. As I’ve written before someplace, it’s the story of a farmer who stays inside when it’s raining and puts in extra hours when the sun is shining.

Well, workers quit when bad technology arrives. What technology would that be? Take a look Paul, when do workers quit? Mostly on the presidential election cycle, every eight years, which one can see by looking at the grey bars in the chart above. So, Krugman tells us the bad technology is the government sector, driving us into bankruptcy. Thanks for the tip, we could never have figured it out by ourselves.

Arnold Kling's version of PSST tells us that we are always in disequlibrium, and so these period crashes are random. How random? Simple computation tells us that this random sequence has about a 1/400 chance of happening.

Soros says not that random. Soros evidently looks at the grey bars, and he just placed an additional 1.3 billion dollar bet that Krugman's bad government technology will arrive within the year.

Don't listen to economists, listen to me, I think Soros does..

Sunday, February 16, 2014

The classic coordination problem

The government sector. We are all realizing the mismatch between the three large sunbelt and the small states. It is being priced in and soon we will adapt, reagglomerate the states and work it out. The key is when Janet restarts QE, then the whole thing becomes obvious, and the distribution stops as gains are impossible and deflation slow tax collections.

California unable to understand banking will not be able to create a new money system. Florida stuck, and the Senate holding the budget hostage. Small states will form regional blocks for political power.

California unable to understand banking will not be able to create a new money system. Florida stuck, and the Senate holding the budget hostage. Small states will form regional blocks for political power.

Oh, Larry, We think we found the source of inequality

America risks becoming a Downton Abbey economy

We think the problem is a skew in democracy making it nearly impossilbe to deliver truth to the middle class. Party oligarchs have masked information from the middle class who are increasingly buried in these increasing large sunbelt states. You, Larry Summers, are part of the problem. You fail to study fair voting and its consequences, which are mainly good.

In Larry's entire career as a bureaucrat, he has never really discovered the necessity of fair voting and the agglomeration problem of large states. A sad work history indeed, almost criminal. Arnold Kling's version of PSST tells us that we are in disequilibrium, so these crashes are just random? No, the probability that this periodic sequence is random is about 1/400.

Inequality has emerged as a major issue in the US and beyond. A generation ago it could reasonably have been asserted that the overall growth rate of the economy was the main influence on the growth in middle-class incomes and progress in reducing poverty. This is no longer a plausible claim. The share of income going to the top 1 per cent of earners has increased sharply. A rising share of output is going to profits. Real wages are stagnant. Family incomes have not risen as fast as productivity. The cumulative effect of all these developments is that the US may well be on the way to becoming a Downton Abbey economy. It is very likely that these issues will be with us long after the cyclical conditions have normalized and budget deficits have at last been addressed.

We think the problem is a skew in democracy making it nearly impossilbe to deliver truth to the middle class. Party oligarchs have masked information from the middle class who are increasingly buried in these increasing large sunbelt states. You, Larry Summers, are part of the problem. You fail to study fair voting and its consequences, which are mainly good.

In Larry's entire career as a bureaucrat, he has never really discovered the necessity of fair voting and the agglomeration problem of large states. A sad work history indeed, almost criminal. Arnold Kling's version of PSST tells us that we are in disequilibrium, so these crashes are just random? No, the probability that this periodic sequence is random is about 1/400.

Saturday, February 15, 2014

Hating volatility

We need some, it is a signal. Who hates volatility the most? Florida, the retirement state, then California by sheer size. Texas at the savings and loan, crisis; Texas now in oil surplus and more neutral to volatility. In these circumstances there is a cost in Federal deficit to keep the small states stable to volatility.

Clinton's revenge was taking the tax quants, leaving California bare, and we ate the volatility. So, what do the small states do without discretionary spending? They get volatility spikes, unfair. Hmmm...

Clinton's revenge was taking the tax quants, leaving California bare, and we ate the volatility. So, what do the small states do without discretionary spending? They get volatility spikes, unfair. Hmmm...

Friday, February 14, 2014

RBC makes a booboo

It is not always this way, sometimes real shocks happen. But you can see that since 1980, the accounting fraud from DC has grown worse, causing various and unnecessary crashes. We know why government does this, they can avoid the pain of real democracy. During crashes, the Fed can bury a lot of the uncovered inflation, for a while. Then government debt buries a bunch more. But the game is over, it is time for DC to pay the price and the cost will likely fall on the small states that control the Senate.

Teeny Tiny Dim Kim Son is at it again

According to the diplomat.

Reports indicate he will also go on a drunken shooting spree.

North Korea appears to be laying the groundwork to begin a new round of provocations, which could very well take the form of a missile and/or nuclear test.

Despite its deliberate (and successful, in the U.S. at least) attempts to portray itself as an irrational actor, North Korea’s provocations usually follow a well-worn playbook. This begins with North Korea mounting a charm offensive that is aimed primarily at South Korean audiences. The purpose of this charm offensive is to create hope that Pyongyang could be turning over a new leaf. Amid this charm offensive, North Korea quietly demands that South Korea and/or the United States do something that Pyongyang knows full well they won’t do. When they predictably fail to meet the demand, Pyongyang insists that it is being provoked, and uses this supposed provocation to justify its brazen actions. This allows North Korea to blame its own actions on South Korea and the U.S., which can be convincing to some audiences in China, South Korea, and even the West.

Reports indicate he will also go on a drunken shooting spree.

What is the definition of easing?

Business Week Sanjay Sanghoee says: