The chart shows the effective interest rates paid by Congress, and falling. Why? Memories are long and the high rates of the Reagan era scare politicians? Maybe. One thing we know is that disinflation has been pushed by the Fed ever since Volker. Mainly, I think, Congress knows that interest expense is volatile and they are very frightened. Something is driving DC and the Fed to keep this interest expense down, this requires some thought.

The chart shows the effective interest rates paid by Congress, and falling. Why? Memories are long and the high rates of the Reagan era scare politicians? Maybe. One thing we know is that disinflation has been pushed by the Fed ever since Volker. Mainly, I think, Congress knows that interest expense is volatile and they are very frightened. Something is driving DC and the Fed to keep this interest expense down, this requires some thought.So lets look at the ten year rate:

Imports bring lower prices and compensate for lower rates. And, at lower bound we have exhausted that resource. What comes next? Well oil prices now stabilize world inflation. As the world demands more oil we accept greater inflation.

Imports bring lower prices and compensate for lower rates. And, at lower bound we have exhausted that resource. What comes next? Well oil prices now stabilize world inflation. As the world demands more oil we accept greater inflation.

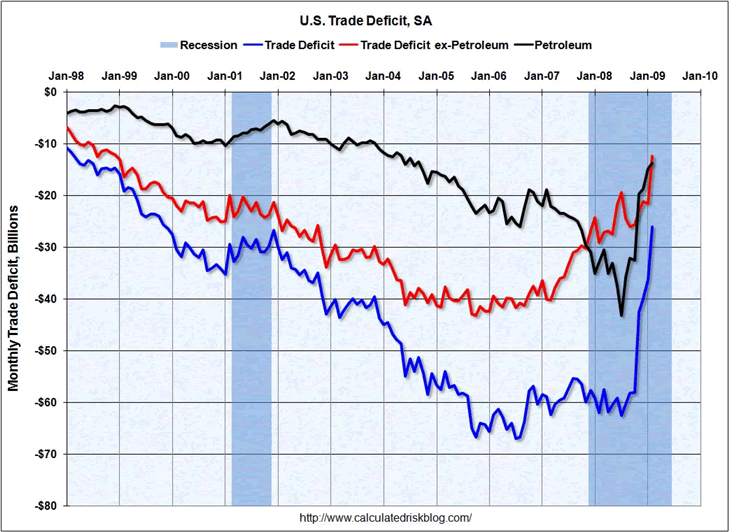

Hence we expect global rebalancing. How is it going?

Deo’s bullet points:

FT Alphaville: Over the past five years there has been a clear inverse relationship between changes in domestic demand and changes in the external balance. With the advent of smaller US external deficits, the rise in foreign official holdings of Treasuries (from $600bn in 2000 to $4,000bn in 2013) has slowed and may even be reversing (with a decline of roughly $125bnbetween March and August 2013). The trade intensity of the global recovery has fallen. Prior to the crisis, a 1 percentage point increase in global GDP growth boosted world trade by roughly 2 percentage points. In the past five years, the trade multiplier has collapsed. Trade is growing in line with sluggish world GDP growth. With domestic demand still skewed towards the US, the UBS paper concludes conclude that: The US is still the sole major economic region capable of driving up its rate of growth via increased domestic demand. If the US is to restore full employment, it will have to do so without much help from the rest of the world. Given that the US economy does not have the same vitality that it did before the crisis, the exported recoveries elsewhere will remain correspondingly weaker for longer.

1 comment:

kd 11 shoes

fitflops sale clearance

converse shoes

mbt

christian louboutin shoes

nike shox

coach handbags

moncler outlet

vapormax

kyrie 5 shoes

Post a Comment