Cambell-Schiller discovered that we are not Guassian random walkers. Who coulda known? Lets look at the results:

Cambell-Schiller discovered that we are not Guassian random walkers. Who coulda known? Lets look at the results:

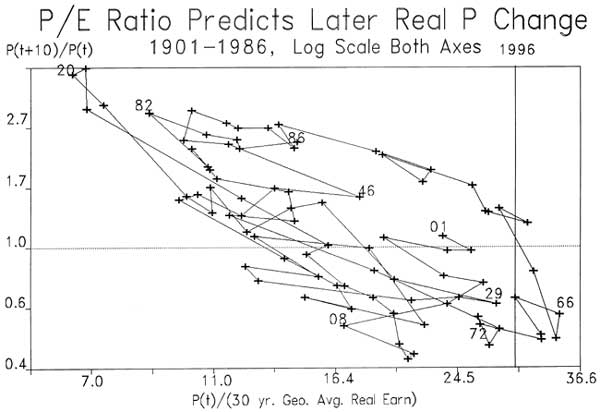

I never understood why the future Price–Earnings Ratios should be compared to the stock price changes over long periods when money is a variable. Schiller needs a ratio on the Y axis, the price of stocks relative to some standard price other than the producer price index. Money is a variable not likely to be tamed by the producer price index.

Schiller is correct to use the producer price index to adjust for inflation as corporations nominally are producers. But exchange rates and sales prices affect the result also.

Schiller is correct to use the producer price index to adjust for inflation as corporations nominally are producers. But exchange rates and sales prices affect the result also.What the chart I posted shows is that as yields and growth have dropped over the thirty years, yet the SP500 still has 500 members, all these members cannot fit on the contracted yield curve, as defined by banks rates. The 'cannot fit' condition is driving the bubble.

So, if we are in an irrational bubble, and Delong notices this, and the stock market tells us they drive up prices because Ben is a pumper, and Delong wants the Fed to pump. How does stock pumping cause the Magical Upturn Cycle?

No comments:

Post a Comment