Years ago I

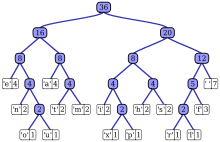

Huffman encoded the SP500, assuming the investor wanted his regular investments to be normally distributed. I got a tree like this:

The weighted nodes told the investor how much money to invest in a particular stock at some price. Probably not optimum but it minimizes transactions and maximizes use of pricing information. Under the assumptions, (−

wi log2 wi), contribution to entropy, was maximally equal for each stock.

Anyway, I am going to do more with this, mainly to try out my favorite tool, wxMaxima.

No comments:

Post a Comment