I can do this by eye. I know that stationary implies the sampling theorem is met, and I look and see that everywhere the lines make a trend, the number of recessions has regularity.

I can do his test by eye because the spectrum is sparse, easy for me to spot the regularities. I am really looking for regularity of zero crossings to determine this meets the sampling theorem; and that is really the test of stationary.

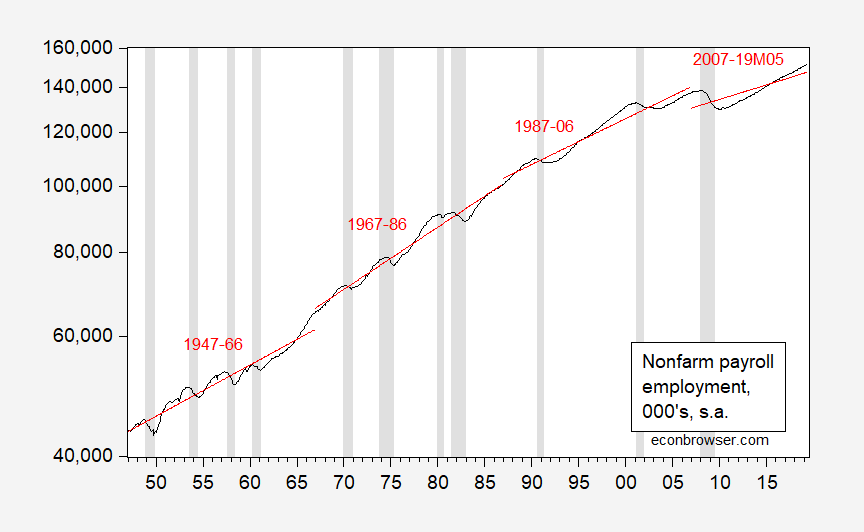

The trend changes because the agents do automatic scale adjustment when the trend fails. That trend is the velocity equation, it is made accurate by scale adjustments, scale adjustments are an altering of the sampling rates on both sides of the trade. AGents are algebraic in pricing, the math equivalent of lifetime hypothesis from Milt. The actual mechanism is deja vu, agents spot peaks in the cycle, identify the complete sequence them rhyme the sequence to maintain velocity. We are a self sampled system, the solution must be quantum mechanical (a spectral packing problem).

This is what sandbox does when it optimizes congestion, tending to change scale in the pits such that velocity equations stay accurate, like a prime number system. The period between trends is the requant where the commutative property is executed by the pit bosses. I am suggesting to economists that this pit boss process be called the Baumol effect, but it is up to them.

No comments:

Post a Comment